Most companies run on annual budgets. A three-month process every fall, assumptions locked in December, a document that gets less accurate with every month that follows. By Q2, the variance analysis is more archaeology than finance.

Rolling forecasts solve this. Not by eliminating the annual budget, but by replacing the part of it that breaks down soonest: the assumption that what you knew in November is still the right guide for decisions you're making in April.

This guide covers what rolling forecasts are, how they differ from static budgets, why they matter for advisory firms delivering FP&A to clients, and what to look for in rolling forecast software.

What Is a Rolling Forecast?

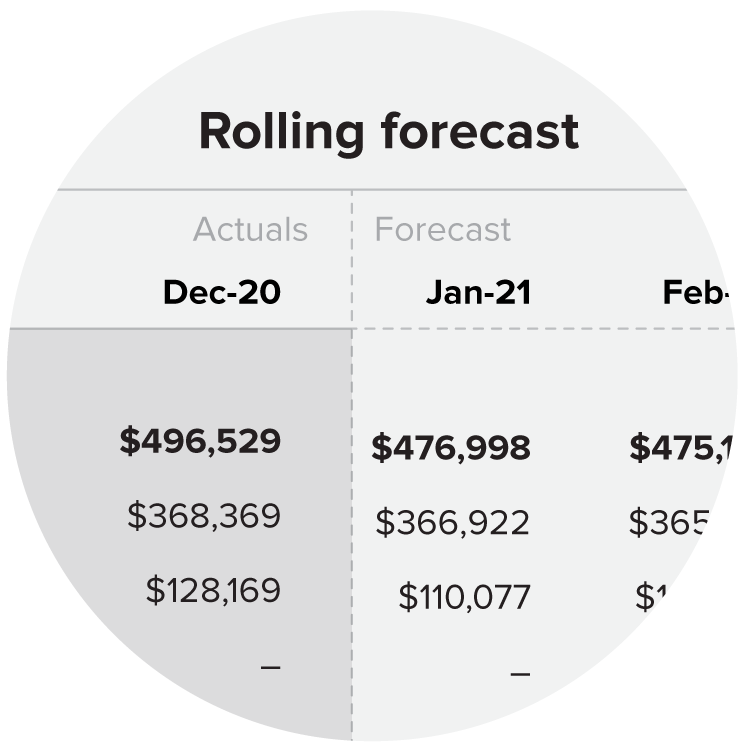

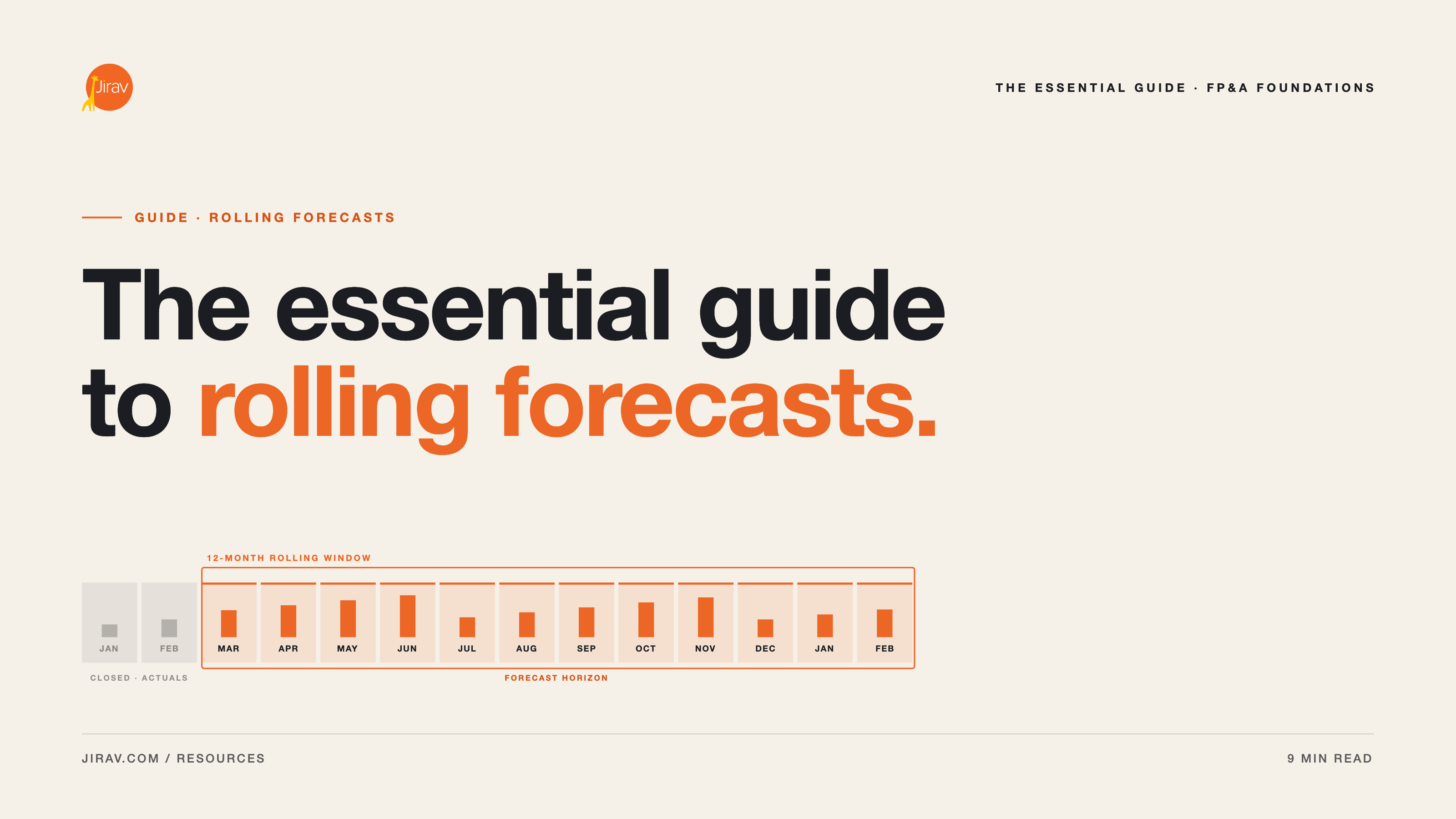

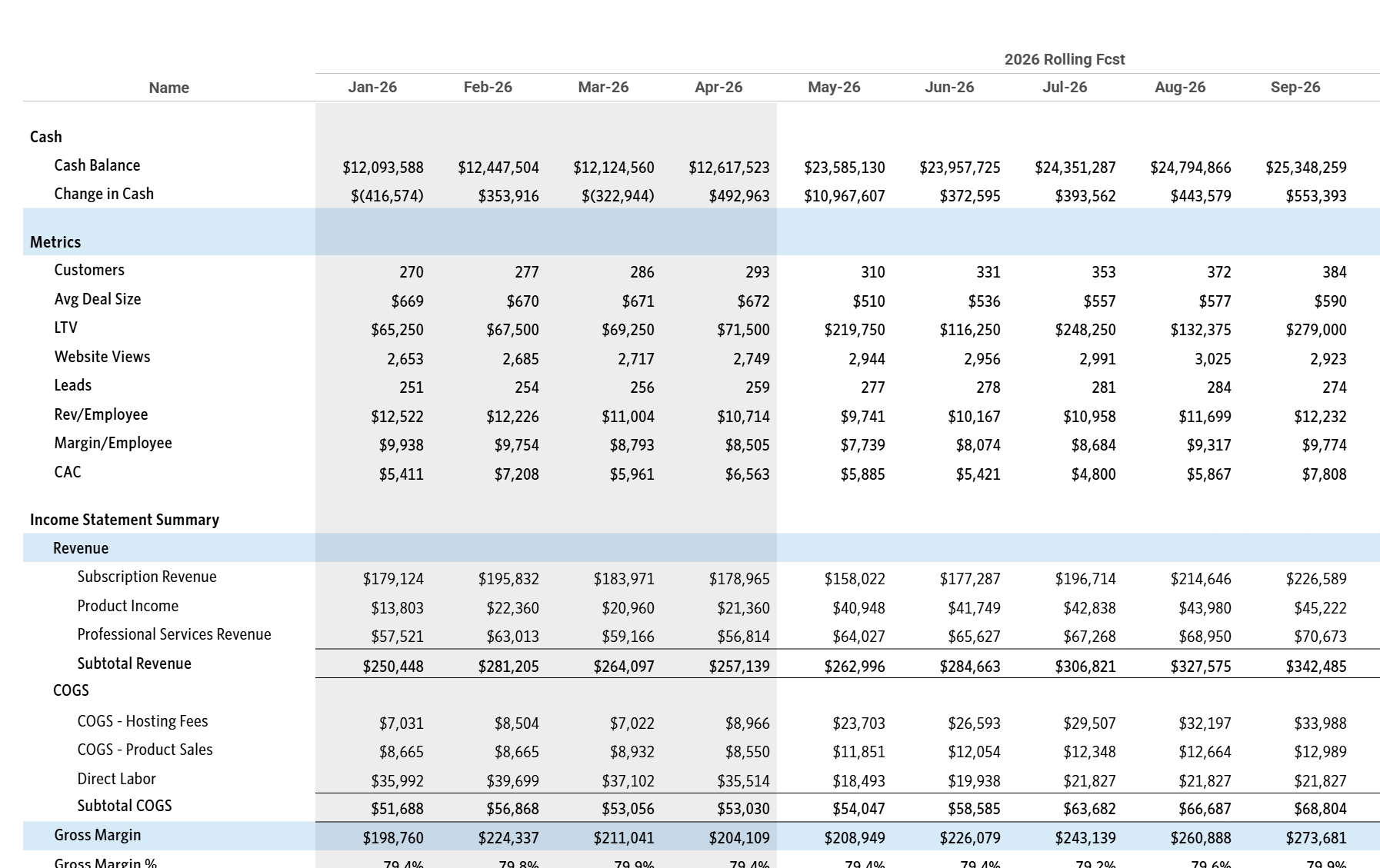

A rolling forecast is a financial planning method that replaces the fixed-period budget with a continuously updated model. As each month closes, that period's actuals replace the oldest forecast period, and a new period is added at the far end. The planning horizon stays constant. The underlying assumptions get refreshed continuously.

The most common configurations are 12-month and 18-month rolling forecasts, updated monthly or quarterly. A firm running a 12-month rolling forecast as of January 1 will, by March 1, have replaced January and February with actuals and added the following January and February as new forecast periods. The window keeps rolling forward.

Rolling forecasts work because they're structured around models, not templates. A static budget is a schedule of numbers. A rolling forecast is a driver-based model where changing one assumption (headcount, pricing, churn rate, deal close rate) flows through the income statement, balance sheet, and cash flow statement automatically. That connectivity is what makes rolling forecasts useful in advisory settings: the model responds to the conversation in real time.

Rolling Forecasts vs. Static Annual Budgets

The practical gap between a rolling forecast and an annual budget opens up fast. Here's where it shows:

Time horizon. An annual budget covers a fixed period. A rolling forecast always extends the same distance into the future. A client making a hiring decision in October is looking at a model that projects twelve months from today, not a December budget with one quarter of runway left.

Update frequency. Annual budgets are built once and checked periodically. Rolling forecasts are updated on a defined cadence, usually monthly, as actuals flow in. The conversation shifts from tracking against a number set eight months ago to reviewing what the next twelve months look like with current assumptions.

Responsiveness to change. Annual budgets lock in assumptions that reflected conditions at the time of budgeting. Rolling forecasts surface assumption drift before it becomes a problem. When a client's revenue mix shifts or a major hire changes cost structure, the model reflects it in the next update cycle, not at the end-of-year review.

Resource decisions. A static budget encourages 'use it or lose it' thinking. If department heads know unspent budget disappears, they spend it. Rolling forecasts support more rational resource allocation because decisions are evaluated against a forward-looking model, not a fixed allocation from the previous fall.

Strategic alignment. Annual budgets often disconnect from the strategic goals that shaped them by the time execution is underway. Rolling forecasts create a continuous feedback loop: goals feed assumptions, assumptions drive the model, actuals update the model, and the updated model informs the next conversation with leadership or clients.

None of this means annual budgets are worthless. The plan of record still matters for performance accountability and board reporting. What rolling forecasts provide is the continuous planning layer that makes the annual budget a useful reference point instead of a constraint that's already out of date.

Choosing the Right Rolling Horizon

Most firms settle on 12-month or 18-month rolling forecasts. The right choice depends on how far out meaningful decisions require visibility and how frequently business conditions change.

12-month rolling forecasts are the most common. They're long enough to plan hiring, capex, and financing decisions, and short enough that the assumptions in the outer months remain reasonably grounded. For most SMB clients, 12 months provides sufficient planning runway without requiring highly speculative projections.

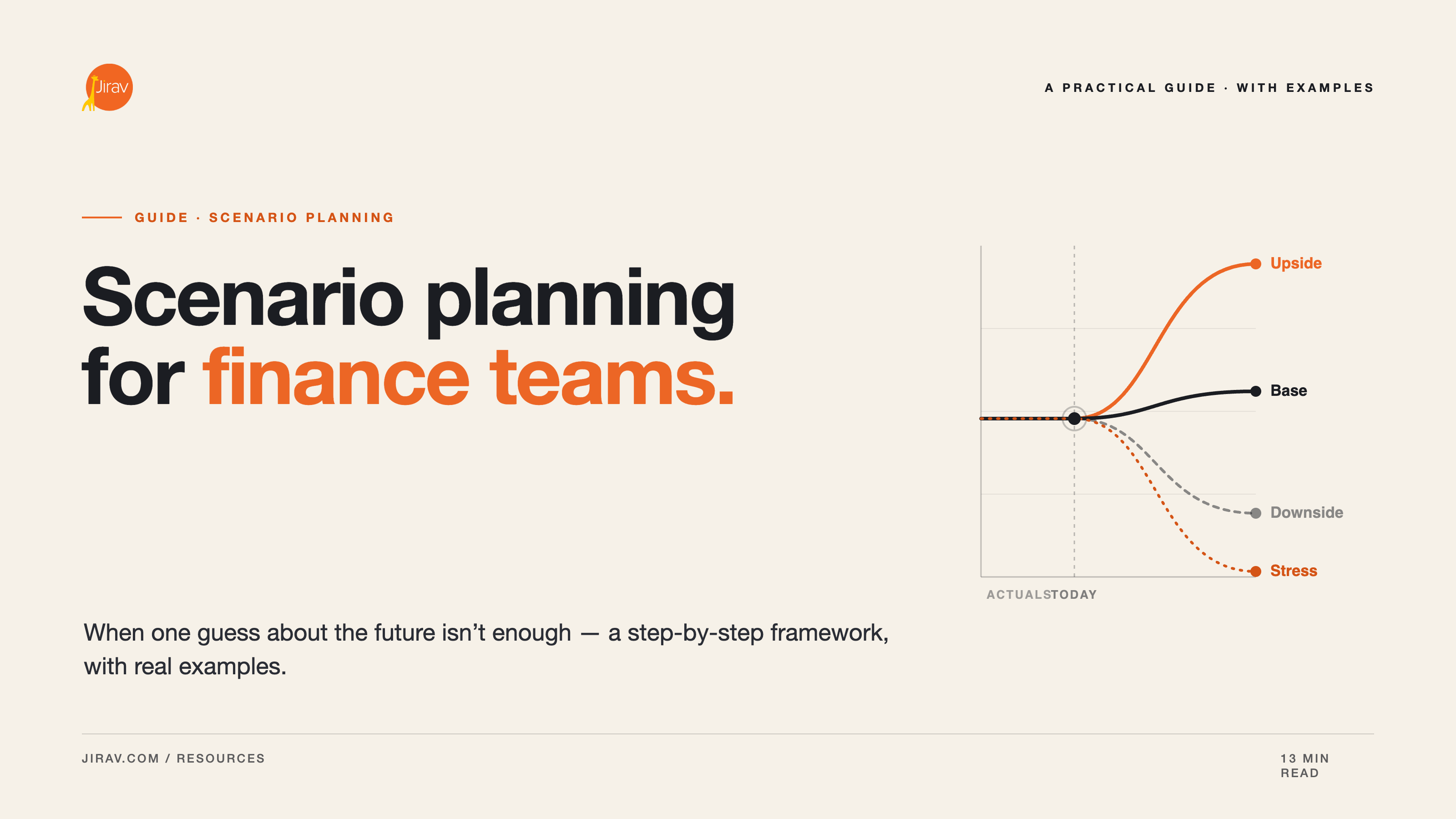

18-month rolling forecasts make sense for businesses with longer lead times: construction and project-based businesses, healthcare organizations planning facility investments, or growth companies with hiring plans that take several quarters to execute. The tradeoff is that outer-period assumptions carry more uncertainty and need to be held loosely.

Regardless of horizon, the update cadence matters more than the length. A 12-month forecast updated quarterly provides less planning value than an 18-month forecast updated monthly. The forecast is only as useful as its freshness.

Why Rolling Forecasts Matter for Advisory Firms

For an accounting firm running FP&A advisory services, rolling forecasts aren't just a planning technique. They're the operational structure of client engagement.

The firms that build strong client retention tend to operate in a similar way. They meet with clients regularly, often weekly or biweekly. Before each meeting, they update the forecast with fresh actuals and review whether the assumptions still hold. The meeting isn't a status report on last month. It's a forward-looking session where the advisor and client work through what different decisions will mean for cash flow, runway, and growth trajectory.

That kind of advisory requires a model that responds in real time. If the advisor exports a snapshot to a PDF, the client can't drill into what drives the numbers. If the model lives in Excel, updating actuals is a manual process that consumes the time it was meant to free up. If the tool doesn't support 3-statement modeling, the cash flow impact of a decision stays invisible until month-end close.

The tools advisors use to deliver rolling forecasts directly shape what's actually possible in those conversations. Firms that systematize rolling FP&A at the model level, not just the reporting level, are the ones that can sustain weekly client meetings without proportional staff increases.

How Rolling Forecasts Work in Practice

A functioning rolling forecast has three components that need to work together:

The Model Architecture

A rolling forecast is built on a 3-statement model: income statement, balance sheet, and cash flow statement, connected so that changes in one flow through the others automatically. Driver-based inputs (revenue per unit, headcount by department, pricing assumptions, gross margin structure) feed into the model rather than hardcoded revenue and expense lines.

The driver-based structure is what makes a rolling forecast different from a fancy budget. When a client wants to explore 'what if we delay this hire by 90 days?' or 'what does our runway look like if churn increases two points?', the model answers those questions because assumptions propagate. Hardcoded numbers don't.

The Rollover Workflow

At the close of each month, three things happen: actuals flow in from the accounting system, the forecast start date advances to drop the closed period and extend the forward horizon, and the advisor reviews assumption drift to flag anything that needs updating before the next client meeting.

This process should take minutes, not hours. If it takes longer, the bottleneck is usually either the data connection (manual export-import from the accounting system) or model complexity (too many nested assumptions that don't cascade cleanly when actuals replace projections).

The Client Conversation

The value of a rolling forecast is realized in the conversation it enables. An advisor modeling live with a client can show the forward cash flow impact of a pricing change, a new product line, or a hiring plan in real time. Clients can see the assumptions driving the numbers, zoom in on specific drivers, and come away with confidence in the output because they participated in building it.

This transparency, the ability to show the math behind the forecast without a fifteen-minute explanation, is often what separates advisory relationships that deepen over time from ones that stall at reporting.

Common Implementation Mistakes

Most rolling forecast implementations fail at the same points:

Building it in Excel. The mechanics that make rolling forecasts useful (automated actuals ingestion, driver-based 3-statement modeling, multi-client template deployment) work against Excel's architecture. You can approximate a rolling forecast in a spreadsheet, but maintaining it across a client portfolio at advisory scale is a manual burden that consumes the time rolling forecasts were supposed to free up.

Designing it as a reporting exercise. A rolling forecast that exists to produce a monthly report is a fancier budget. The value is in the model's ability to respond to changing assumptions. If advisors can't make changes and immediately see the downstream impact on cash, the forecast isn't doing advisory work.

Treating the rollover as a manual step. Some firms build a technically correct rolling forecast but spend two to three hours each month rolling it forward manually. At that point, the capacity cost of the rolling forecast starts to offset its advisory value. The rollover process needs to be automated.

Overcomplicating the model. Rolling forecasts with hundreds of line items and deeply nested assumptions become brittle. They're hard to update, hard to explain to clients, and prone to breaking when actuals diverge from projections. Simpler models with well-defined drivers are more durable.

Skipping the assumption review. Ingesting actuals isn't the same as updating the forecast. A rolling forecast that absorbs new actuals without reviewing whether the underlying drivers still hold will compound stale assumptions forward. The monthly rollover should include an explicit check of key assumptions against recent actuals.

Rolling Forecast Software: What to Look For

The right platform for rolling forecasts at an advisory firm needs to handle a few specific workflows well:

Automated actuals ingestion. Actuals need to flow in from the accounting system without manual export-import cycles. That means native integrations with QuickBooks, Xero, Sage Intacct, and NetSuite, with nightly syncs or better. Any system that requires advisors to manually update actuals every month is adding cost, not removing it.

3-statement modeling. Income statement only isn't enough. Clients care about cash flow and balance sheet health. A model that connects the P&L to the balance sheet and cash flow statement can answer the questions that matter most in advisory conversations.

Automatable rollover. Setting a plan to roll forward automatically, updating the forecast start date, and flagging assumption drift for review should require minimal manual intervention. The advisor's job is the conversation, not the mechanics.

Multi-client template management. Firms serving multiple clients need to standardize model architecture without rebuilding from scratch for each engagement. The ability to create templates and deploy them across the client portfolio is what separates a scalable advisory operation from a custom engagement shop.

Client-facing transparency. If advisors are modeling live in client meetings, the interface needs to be navigable by someone who isn't a financial professional. Clients need to see what's driving the forecast and drill into specific assumptions without needing a guided tour.

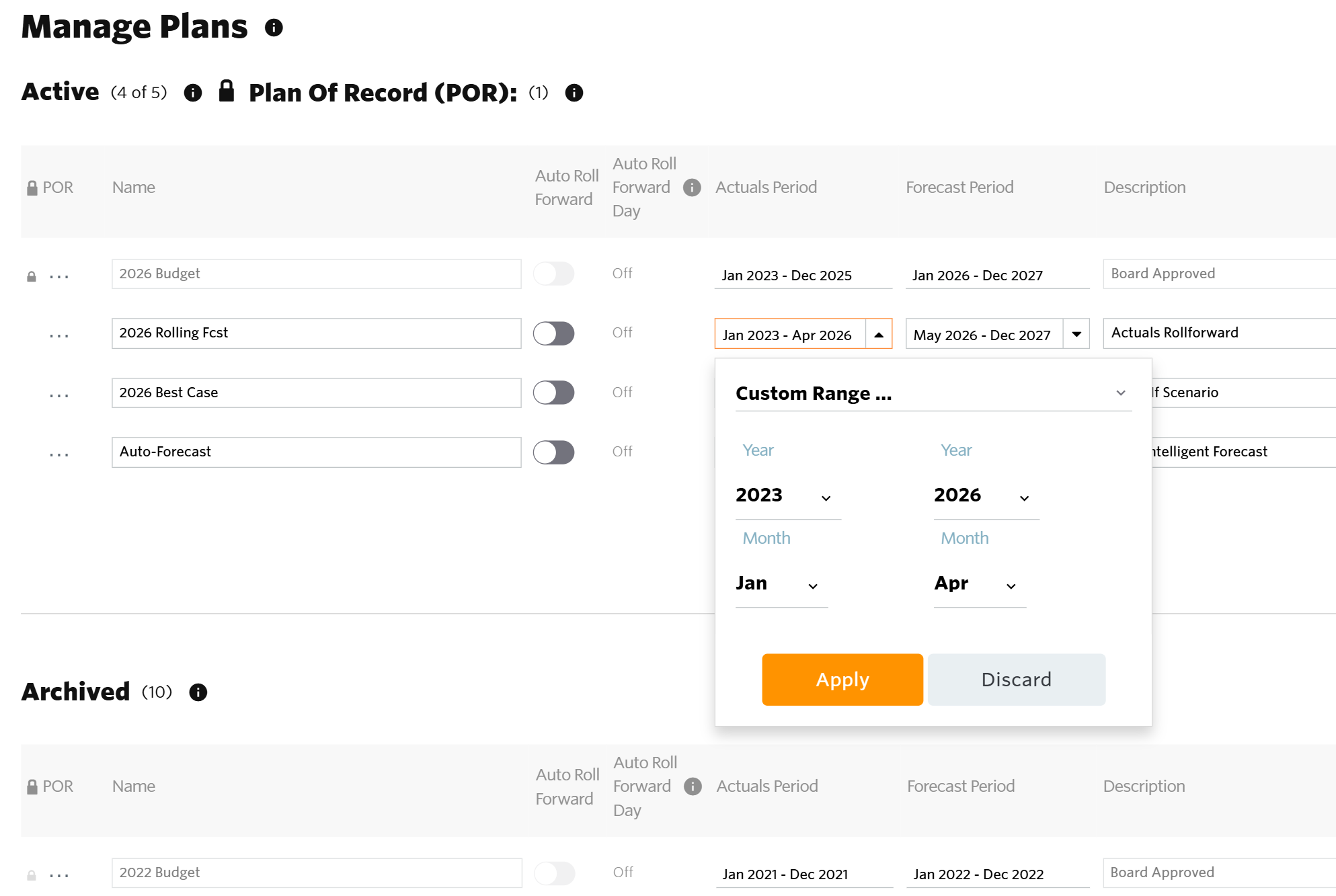

Jirav is built specifically for accounting and fractional CFO advisory practices. The planning and budgeting module supports driver-based rolling forecasts connected to all three financial statements. Auto Forecast uses historical data and seasonal trends to generate forecast starting points, which advisors refine with client-specific assumptions. Plans can be configured to roll forward automatically as actuals are ingested through integrations with QuickBooks, Xero, Sage Intacct, NetSuite, and other connected systems.

For firms managing rolling FP&A across multiple clients, Jirav's client entity structure is designed for that workflow: standardized model templates deployable across the book of business, separate advisor and client-facing views, and reporting packages that can be generated and shared in a few clicks.

If your firm is delivering rolling forecasts manually or looking to standardize rolling FP&A as a repeatable service, request a demo to see how Jirav handles it with your client portfolio.